Are Oil Markets Lying to Themselves (and to the Rest of Us)? You Can Bet On it.

While buyers struggle to source actual barrels of oil, the market is assuming supply will normalize in the near future. Expect that lie to be shattered, and soon.

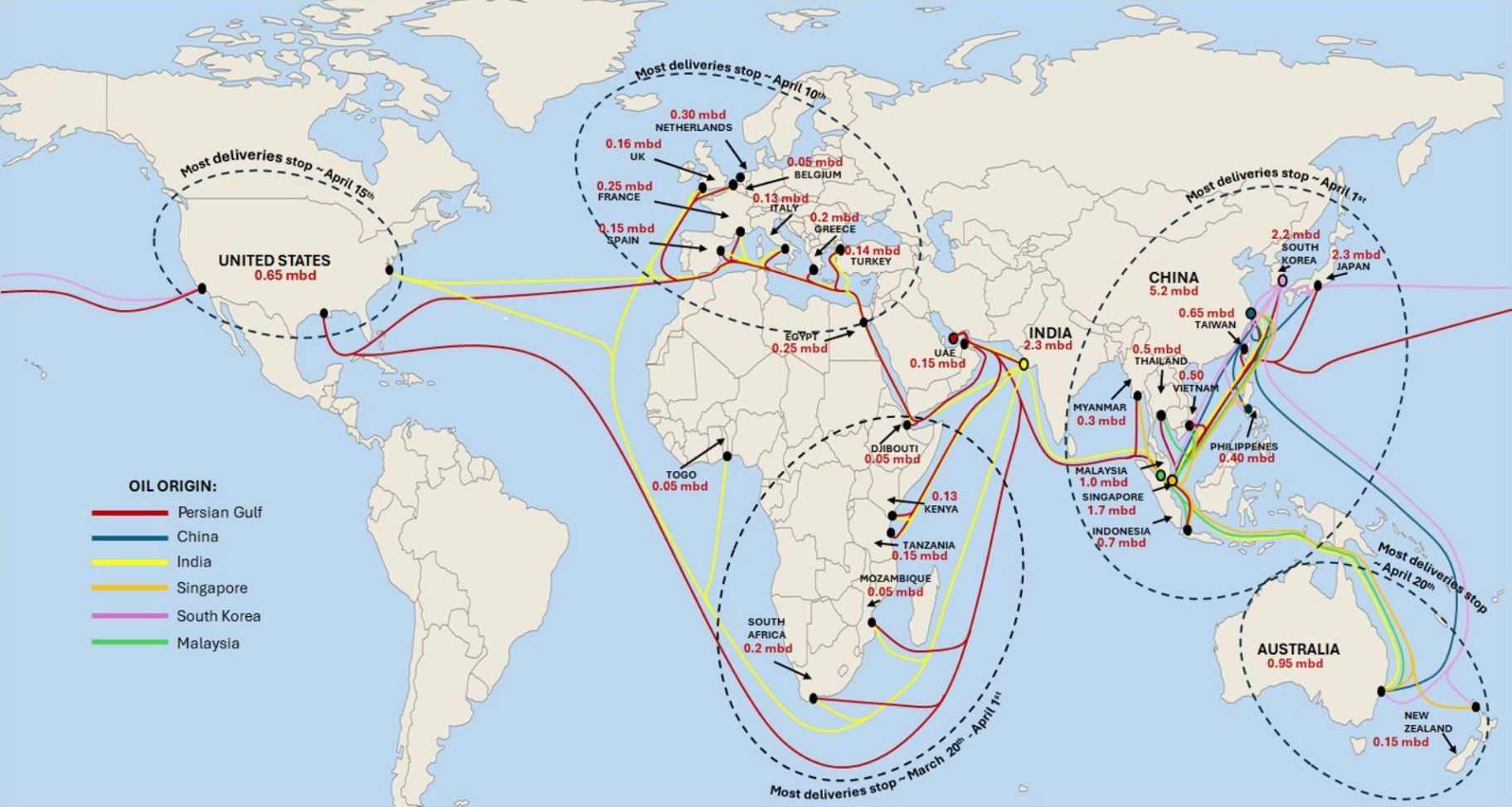

If you think that repercussions from this American attack on Iran haven't turned out to be all that bad, be patient. Cause you can be rest assured that the situation is going to get monumentally worse as the tail end of the conga line of oil tankers that passed through the Strait of Hormuz on February 28th hits its final destinations in the next few days. Once that pinch point is reached refineries will soon thereafter run out of stock and the knock on effects will start coming into play. Recession, deprivation, famine... the way things are going this one's likely to see the whole gamut, and the longer the air pocket of tankers lasts, the worse it's all going to get.

To be clear, what's going to hit won't merely be an oil shock, but rather a full-spectrum commodity shock that'll hit all aspects of our societies – not just fuel but also fertilisers (food), helium (microchips), aluminum (vehicles, power grids, packaging), sulphur (processing of critical minerals, including for lithium batteries), plastics (just about everything), and more.

While the calm and collected reporting by television news programs and the like are by nature effectively downplaying the issues and sedating the public by treating the situation as something akin to a strange curiosity, markets are taking the distortion more than a step further via their concerted aversion to pricing in what's so far been little more than the early stages of the oil shock portion. To understand this diversion one needs to understand a bit about the way in which oil is bought and sold.

When one hears news programs and the like talking about the price of oil, it's all but certain that what they're referring to is the price of one of the world's two main benchmarks for crude oil: Brent (named after the Brent oil field in the North Sea) and WTI (West Texas Intermediate). In short, while Brent's North Sea origins translate into it standing for waterborne oil that's easy to ship (pricing about two-thirds of the world's internationally traded oil), WTI finds its origins in the United States and so refers to landlocked oil that relies more so on pipelines. The occasional price spread one might see between the two is due to their differing qualities, transport costs, and sometime oversupplies, and while Brent is generally seen as the "world price" of oil (with greater exposure to international disruptions and shipping), WTI is generally seen as the "US price" (reflecting American production and demand).

While there's dozens of other benchmarks for various grades of oil originating in various parts of the world, the other key benchmark relevant to this piece is known as Dated Brent. Dated Brent, consisting of a basket of crudes (Brent, Forties, Oseberg, Ekofisk, Troll, and WTI Midland), is the global benchmark for physical crude of which not only gets assessed daily by agencies such as Platts, but which is based on trades of actual physical oil and so represents real-time cargo availability. Brent and WTI, on the other hand, are crude futures based on paper contracts. They're financial instruments traded on the Intercontinental Exchange (ICE Brent) and the New York Mercantile Exchange (WTI). Brent and WTI don't so much represent actual barrels of oil so much as they are bets on barrels of oil. Brent and WTI are effectively appendages of the futures market (a centralised financial exchange where standardised contracts are bought and sold for the delivery of assets at a set price on a predetermined future date) and are nothing more than a reflection of what investors and markets think the price to be months down the road (say, for June delivery or July delivery or what have you).

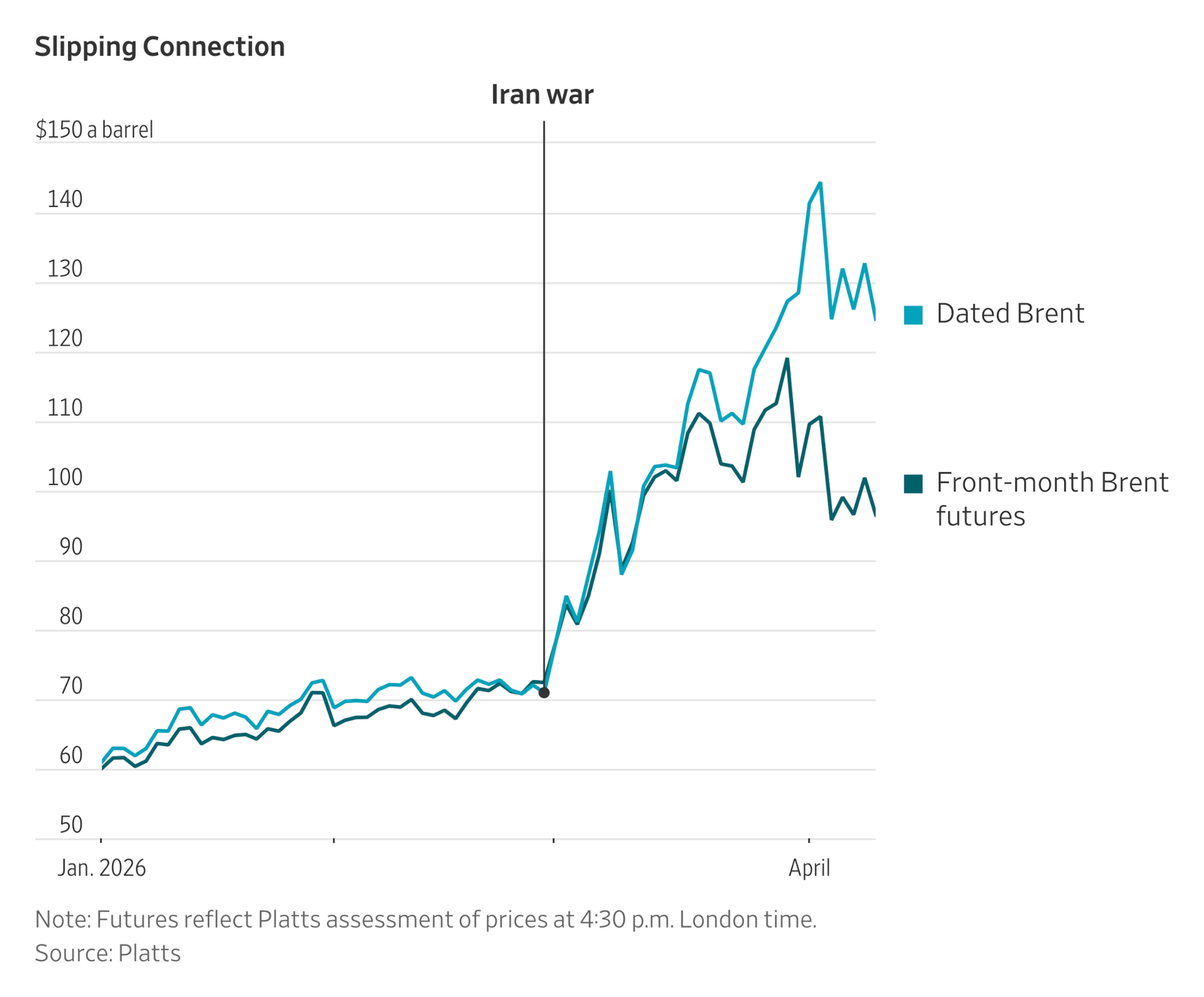

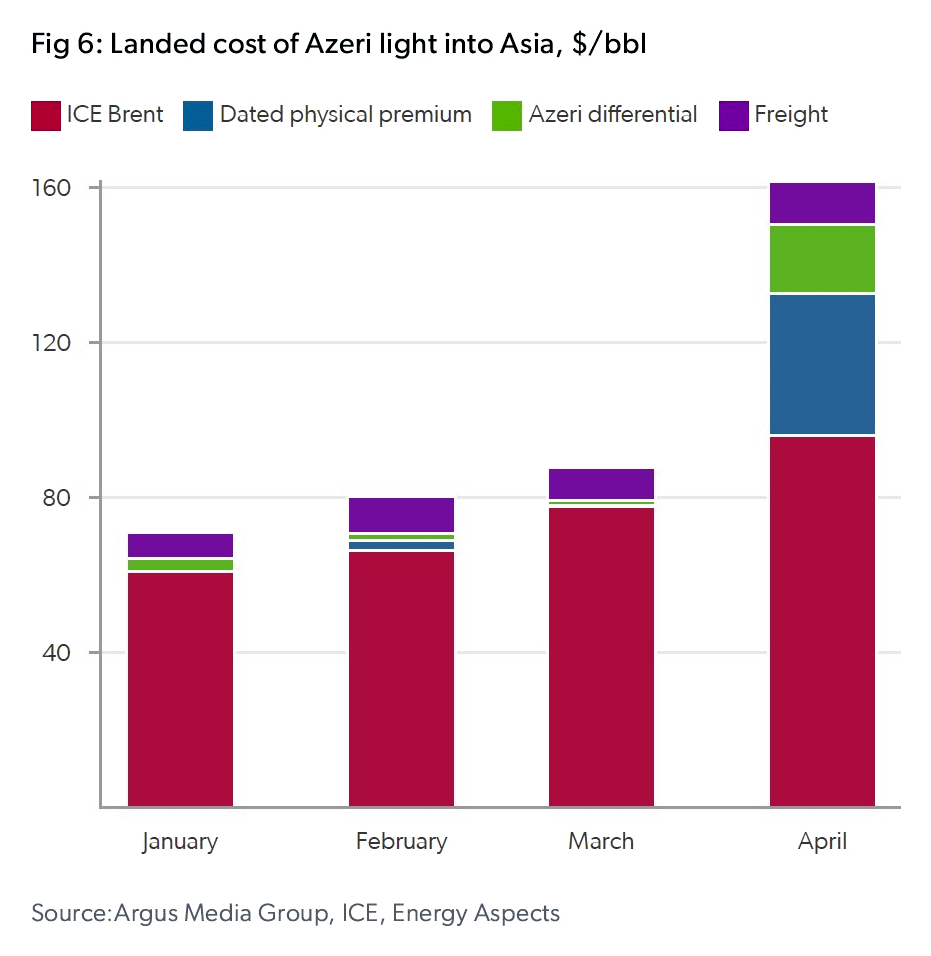

While the spread between the Brent and Dated Brent benchmarks has historically been between $1 and $2, something strange started happening with the price differential between the two come mid-March. That is, although Dated Brent continued on the steady upward march it had embarked upon following the attack on Iranian officials on February 28th (resulting in its price pushing $150 at one point), Brent on the other hand was more hesitant in its increases. Although Brent did make a few forays above $100 – including a high of $119.50 – it generally made its way back to $100, +/- $5 or so. A roughly $30 spread emerged between the two (Figure 1), a gap that's never been seen before.

We won't delve in this piece into the main culprit(s) driving this pricing differential, but will instead look at the fact that the global energy shock has yet to be priced in. As International Energy Agency head Fatih Birol recently stated at an Atlantic Council forum,

Prices are already high, but they are not reflecting the severity of the problem — I agree there is a disconnect. But I think soon we will see they will converge, which is an extremely sensitive issue for the global economy.

In short, the gap between the prices for physical oil and paper oil is effectively the size of the lie the market is telling itself (which is essentially that this is basically all over or at least rolling over), seen by the way in which buyers are struggling to source actual barrels of oil while the market is effectively assuming supply will normalise in the near future. The deception is an outcrop of the fact that markets have an ingrained predisposition to living in the fantasy world of pining for the stability of the status quo to remain in perpetuity, precisely so that in one way or another profits can continue to be made (premised on there being actual goods and services that can be purchased with those profits). Put a bit differently, "smart" traders are able to make money off of fools who believe the promises of the orange guy with frontotemporal dementia.

In effect, while the market is trading the ceasefire and whatever else comes out of the pie hole of the frontotemporal dementia-ridden orange guy, the physical oil market is reflecting actual supply shortages. Refiners in places like Singapore, Japan, China, South Korea and India are bidding up cargoes due to the scarcity of actual barrels available for loading in the Gulf, pushing spot prices to levels that reflect the severity of the supply crisis.

The spot price of oil, for those unfamiliar, is understood as the current market price for immediate purchase, payment, and delivery of a physical barrel of crude oil, reflecting instant demand and supply (with delivery often occurring within a few days), as opposed to futures contracts which lock in prices for future dates. Dated Brent isn't regarded as spot, although the aforementioned (North Sea) Forties, a major component of the Dated Brent assessment, generally is. And although Dated Brent (which Brent is a part of) dipped in price alongside Brent (Figure 1) when when the frontotemporal dementia-ridden orange guy unilaterally announced the conditional ceasefire with Iran on April 8th, North Sea Forties didn't budge.

That is, the physical market took a look at the ceasefire and didn't buy it for a second. Traders who buy actual barrels of oil and sell them to actual refineries – and whose livelihoods are based on whether ships actually reach port – maintained their war-premium bids while the futures market pulled out the champagne bottles. A few days later, when the talks in Pakistan fell apart, the physical market was effectively proven right while the market was proven wrong.

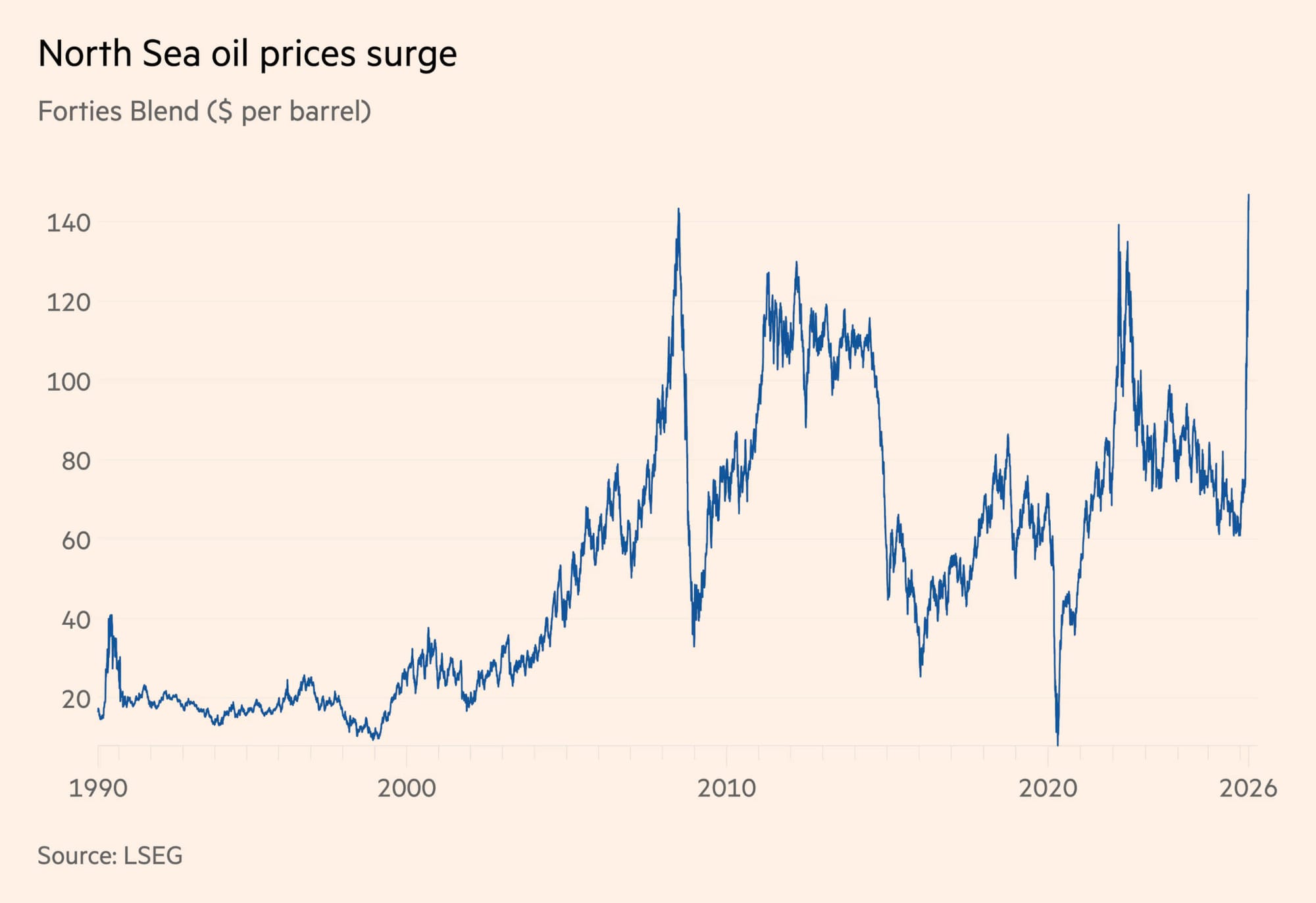

However, although North Sea Forties reached – and stayed at – a price about $50 higher than Brent, that's not to say, as Reuters did, that "The outright price of North Sea Forties crude reached $148.87 a barrel on Monday, LSEG data showed, exceeding its 2008 peak". First off, those $148.87 were actually more like $160 if freight was counted, which is also rapidly increasing due to higher bunker fuel prices whose supply may even run out and cause container vessels and bulk carriers to halt in some parts of the world.

But secondly, and more to the point, although Brent did in fact hit a peak of $147.50 in July of 2008 and so was bested with the recent $148.87, when adjusted for inflation those 147.50 in July 2008 dollars would be roughly 225 in today's dollars.

In other words, while the price of Brent and WTI may very well be getting repeatedly talked down so that headlines can continue with their calming sentiments and so that prices can stay below the psychological barrier of $100, once settlement rules and market arbitrage result in pricing convergence between paper barrels and physical barrels, between Brent and Dated Brent (meaning Brent goes up, not Dated Brent goes down), the prices seen on those cute Bloomberg terminals could end up not only reaching the ~$150 levels currently seen via North Sea Forties, but July 2008-matching inflation-adjusted levels of ~$225 or higher. Which would send the world economy into a frenzy, to say the least.

And that's not mere hyperbole, The Financial Times reporting the other day that the highest price (including shipping and insurance) that the CEO of HSBC had seen a barrel of oil go for during this crisis was a whopping $286. It's doubtful WTI and/or Brent would actually reach that high, as long before either benchmark hit that level (which would take a fair amount of time) the global economy would experience one of its greatest crashes ever.

Whatever level of pricing it is that Brent and WTI and all the rest of them end up reaching, the real make or break question is "Who will end up getting a hold of the scarce barrels, whatever the (more costly) price be?" For as energy investor Eric Nuttall recently stated, the world should brace for "significantly higher prices" as "the battle for the physical barrel has begun".

With "the battle for the physical barrel" getting coupled with shortages of fuels for vehicular travel, grounded flights due to scarce jet fuel, and all the rest of it, the facts of the matter are that we can't manipulate our way out of this supply crisis and that physical realities will eventually hit. Unavoidably, it's only a matter of time then before demand destruction kicks in and ruthlessly "sorts things out". That might be another topic for another time.

Comments