Investors and their Wishful Thinking Have Led Us All to Fantasies of a Quick Return to Strait of Hormuz Normality

For a few months now the consensus amongst many powerful firms & institutions is that the SoH would reopen in June, the world thereafter returning to normality. But with that fallacy now disproven, it's time to consider the possibility that the SoH might remain closed for months, even years on end.

It's no secret that as societies we've become dangerously accustomed to just-in-time logistical systems in which materials and products are provided by hyper-efficient supply chains, systems which themselves are dependent on the status quo of business as usual. Looking back just a few years, the bubble of our normalcy bias was somewhat burst courtesy of the supply chain chaos witnessed during the SARS-CoV-2 pandemic, a situation that made it readily apparent that just-in-time logistical systems are precariously vulnerable to disruption.

It would seem though that investment banks and the like are addled with short memories (along with an apparent inability to interpret the facts in front of them), what with their current reaction to this Strait of Hormuz crisis being one in which problems within the energy system are expected to be conveniently rectified "just in time", allowing for the status quo of business as usual to be maintained and for economic conditions to effectively return to how they were back in the (relatively) halcyon days of 2025. Although this piece (published on June 1st, which will be increasingly relevant the further one reads) won't delve into the details of why a near-term resolution to the Strait's status is all but impossible (as impossible as the notion that oil exports from the Middle East, via the Strait, will ever go back to "normal"), the extremely short explanation is that insurance issues, mined waters, operational/logistical problems, and two deadlocked sides unwilling to back down mean that shipping will likely be constrained for the rest of 2026 and, at best, most of 2027.

That all being so, just like the SARS-CoV-2 pandemic resulted in most people and institutions being incapable of accepting that the more predictable and less chaotic days of 2019 were never coming back, with this Strait of Hormuz crisis we can now add investment banks to that list of people and institutions that are similarly failing to accept – or to even recognize – that the relatively stable days of 2025 are never coming back either, be it in the short term, the long term, or even ever.

Goldman Sachs

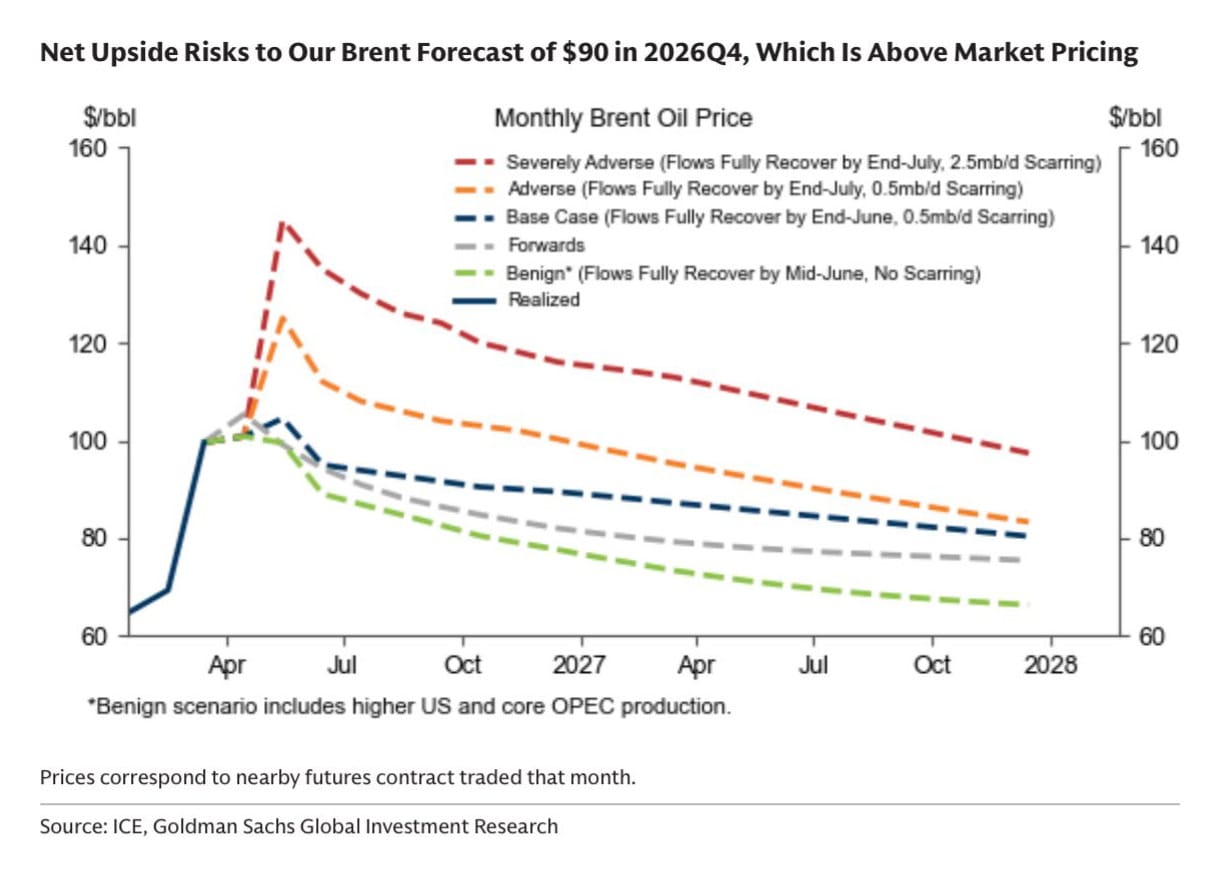

The first case in point would be investment bank Goldman Sachs, which on April 26th published their latest oil forecast, a forecast cognizant of the estimate that Middle Eastern oil production was down by an average of 14.5 mb/d for the month of April. With the price of Brent being about $100 per barrel on the day of publication, Goldman Sachs raised its outlook for oil prices for the second straight month, extrapolated through four scenarios for Q4 2026. In short, the longer Iran's blockade lasts, the more that permanent reductions ("scarring", caused by damaged wells, lost reservoir pressure, deteriorated infrastructure) will occur with Gulf oil production.

- Benign: The Strait of Hormuz is immediately reopened and Gulf exports normalize by mid-June. Capacity isn't reduced, and Brent averages just under $80 by Q4.

- Base Case: Gulf exports normalize by late-June. Capacity is reduced by 0.5 mb/d, while Brent reaches a high of $120 before averaging just over $90 by Q4 and $80 by the end of 2027.

- Adverse: Gulf exports don't normalize until the end of July. Capacity is reduced by 0.5 mb/d, and Brent averages just over $100 by Q4.

- Severely Adverse: Gulf exports similarly don't normalize until the end of July. The difference, however, is that capacity is persistently reduced by 2.5 mb/d, resulting in Brent reaching $140 by June and averaging nearly $120 by Q4.

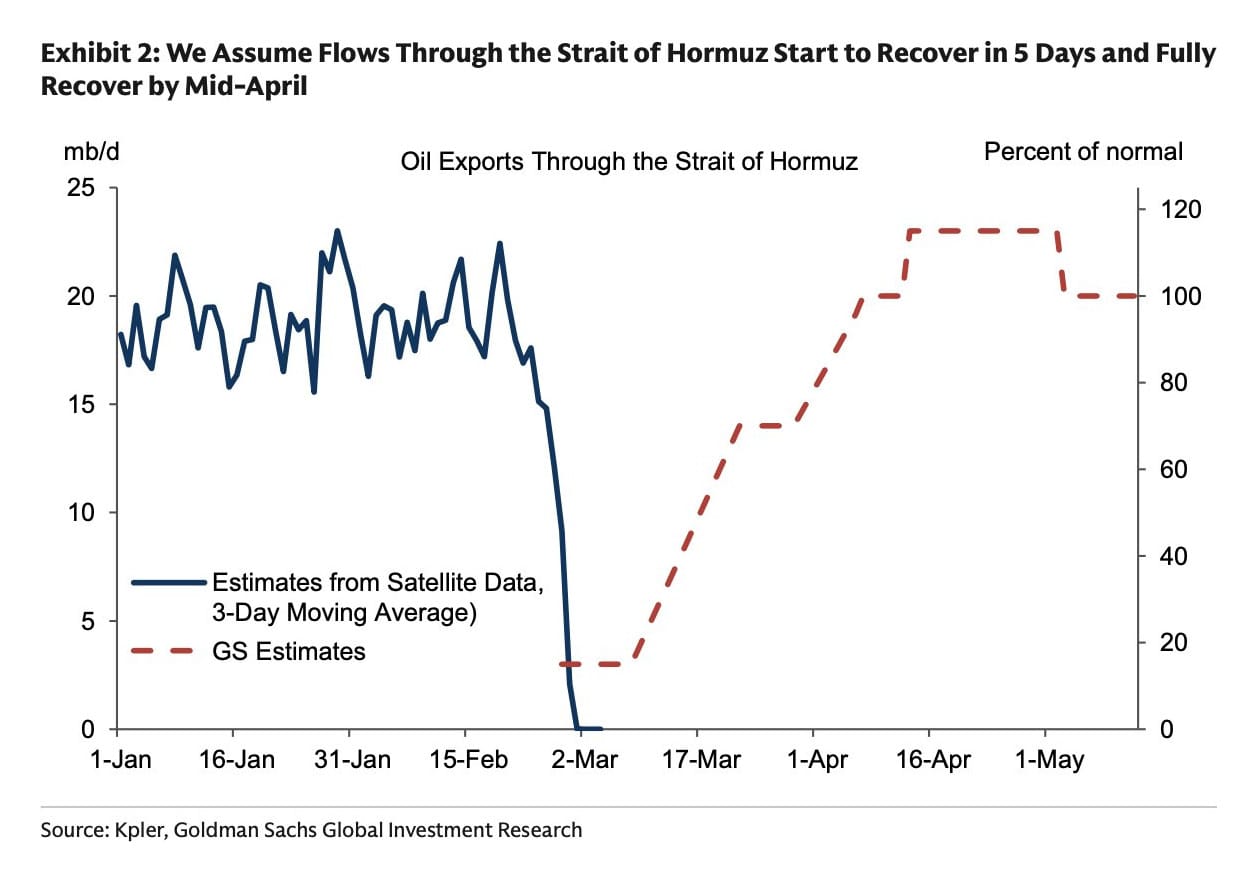

This attitude of "we're just on the cusp of normalisation" easily comes off as rather disingenuous if not just ludicrous, what with Goldman Sachs having made the assumption in the first week of March that traffic through the Strait of Hormuz would begin to recover within days, followed up with full normalisation by mid-April. That, of course, didn't quite happen.

Goldman's blatant delusion in assuming that full normalisation would be achieved by mid-April, generously chalked up to normalcy bias, is enough to make one wonder what the point of listening to outfits as such is when all they seem to be doing is offering predictions of what the timeline to normalisation may look like depending on whether fairy tale #1 or fairy tale #2 comes to fruition. Because as more recently stated by Goldman Sachs,

[A]lthough markets are looking through any temporary disruptions, it may also be that another bout of market worry is needed to force an agreement that allows oil flows to resume.

In other words, the geopolitically-bereft rationale of this multi-billion dollar investment bank is that the situation has to be rectified (in order to facilitate the existence of an environment perpetually conducive to the insatiable desire for relatively predictable profit-making), therefore the situation will be promptly rectified.

Easy!

JP Morgan

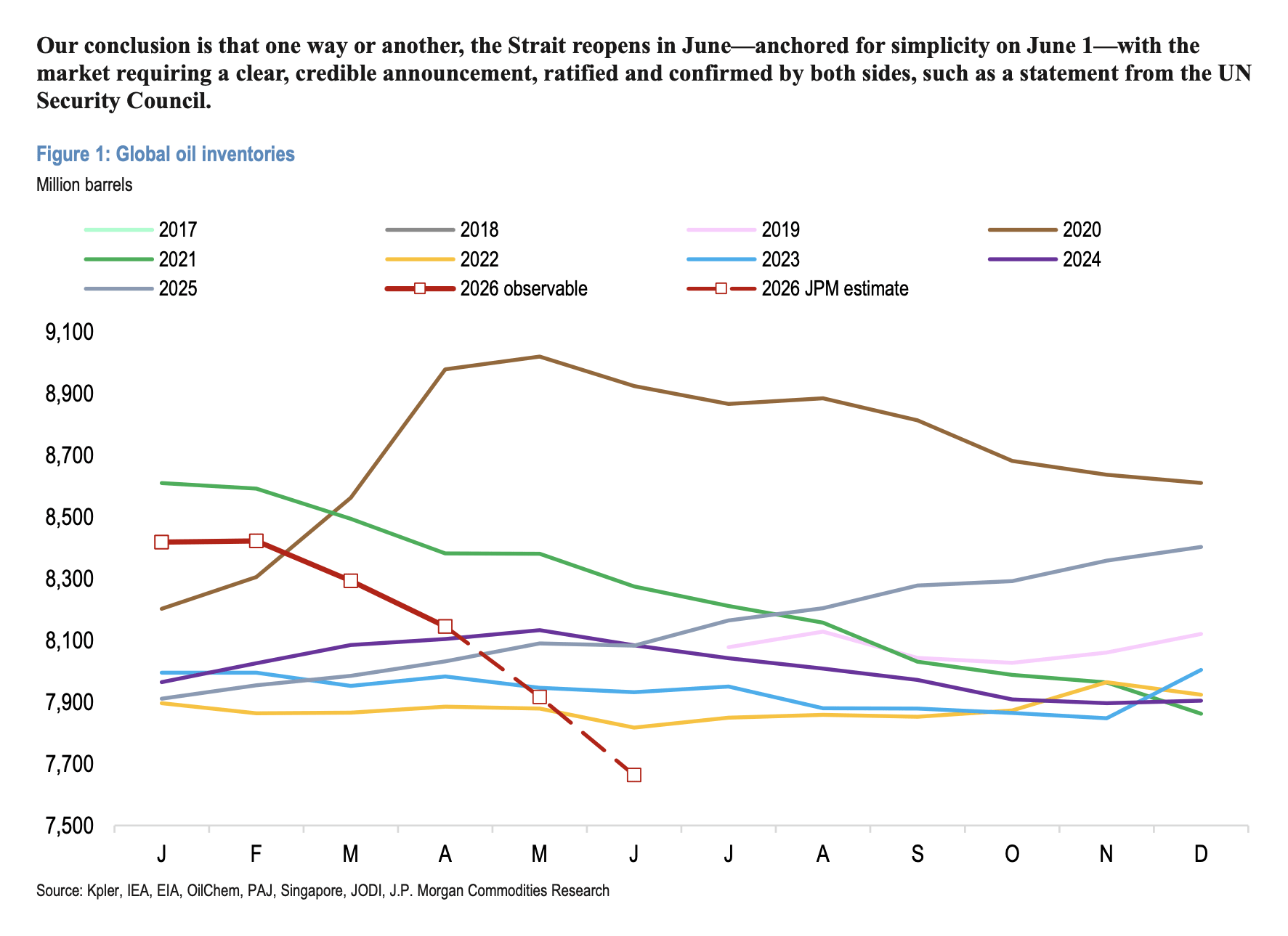

As horrid as Goldman Sachs' takes are there's no need to pick solely on that single outfit, because in early-May the financial services firm JP Morgan similarly concluded that, due to little more than the sheer seriousness of the situation, the Strait would reopen sometime in – you guessed it – June (and more specifically, June 1st, today).

A core assumption of our framework is that the accelerating pace of oil inventory depletion will ultimately force the reopening of the Strait of Hormuz, one way or another. Our base case envisions the Strait reopens in June – anchored on June 1 for simplicity – following a clear and credible announcement ratified and confirmed by both sides, such as a statement from the UN Security Council.

Translated over into plain-speak: "Due to our expectations of reality, we can't possibly accept that the global situation could deteriorate to such unsavoury conditions that life as we've become accustomed to would be put in jeopardy, implying that rational people will therefore step in to make sure the situation is rectified – at worst – just in the nick of time".

Morgan Stanley

Rounding out the Three Amigos (or Three Stooges or whatever you want to call these outfits off in la-la land), the estimated-in-mid-May base case of investment bank and financial services firm Morgan Stanley, according to Bloomberg, just so happens to also be that the Strait reopens in none other than... June.

The path matters: a reopening in June with US and Chinese buffers still partly intact is the base case; a closure that runs into late June or even July is the regime in which Brent flat price has to do work it has so far been able to avoid.

In other words, Morgan Stanley's oh-so-unique base case scenario is that the Strait will open just in the nick of time, before the US needs to cut back on its highly-increased exports and before China decides to renege on its drop in imports (what Morgan Stanley calls "a race against time"). Moreover, and pretty much on par with Goldman Sachs' base case scenario, Morgan Stanley sees Dated Brent averaging $110 over the current quarter, $100 in Q3, and a comforting $90 in Q4 of 2026.

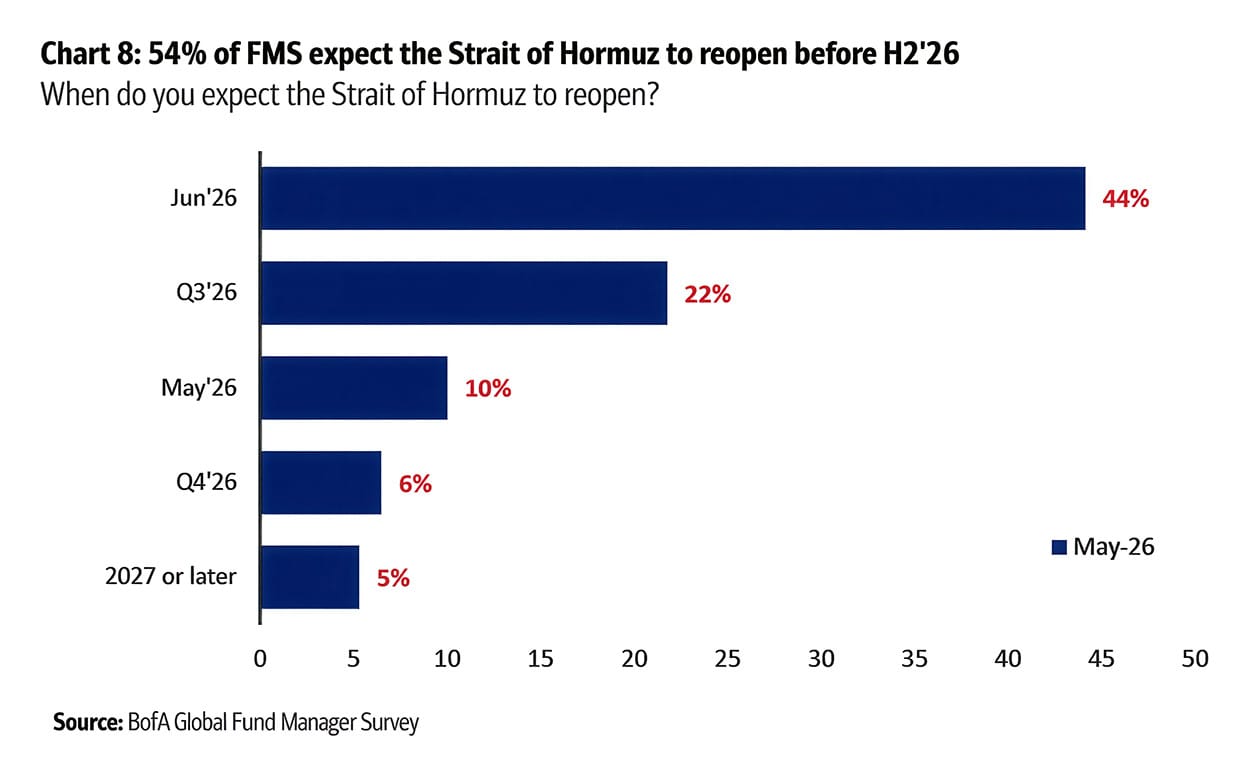

Bank of America Global Fund Manager Survey

Goldman Sachs, JP Morgan and Morgan Stanley aren't the only ones afflicted with some kind of psychological disorder, what with a full 44% of global fund managers surveyed by Bank of America believing – as of mid-May, and with all the evidence readily laid out before us all to peruse over – that the Strait of Hormuz will reopen sometime in June (to go along with another 10% holding the absurd belief that the Strait would open some time later in May).

Fancy outfits, fancy models, high fees

If any of the above modelling (which effectively means all of the modelling, since they're pretty much all identical) and survey results come off as flaccid BS analyses that emerged as the product of a grand circle jerk in which all three firms/banks (and surveyed global fund managers) couldn't give a rat's ass about the validity of the nonsense they spout, you're probably not too far off the mark. For as one Middle Eastern executive is quoted in The Financial Times as having stated at this year's Milken Conference at the Beverly Hilton earlier this month,

The stock market doesn't care about the war.

Sure, the fact that the stock market is reaching record highs can undoubtedly give the impression – to those ignorant of the fact that physical realities matter for the economy – that nothing matters other than hype and ensuing profits.

However, what's more relevant for present purposes is another quote that also derives from this year's Milken Conference, a quote in which a high-powered banker effectively questions if anyone (read: any financial elites) really cares whether or not hundreds of millions of people will have their lives thrown into disarray, and whether or not there's any concern that millions of people may very well end up dying from famine.

Does anyone really care if the Strait of Hormuz is open?

In short, a perfect encapsulation of not just the complete lack of concern for anything other than their personal profit-making opportunities, but also of the motivation behind the analyses by Goldman Sachs, JP Morgan, and Morgan Stanley.

As is abundantly clear, all these analyses assume a short war, albeit for no outwardly obvious reason discernible to the layman. For when it comes to the sell-side community (financial institutions and professionals that create, promote, and sell securities and investment services), the assumption of a short war – i.e. an imminent return to a fair degree of normality – is necessary if one is to adequately assess how to underwrite energy stocks. Otherwise put, while all the aforementioned analyses are exactly what's needed for facilitating a stable environment for investing gambling in energy stocks, they're all the while completely useless when it comes to discerning where oil prices are headed, what the economy might look like in the near future, and what might happen to people's lives and livelihoods.

Simply put, fancy outfits like Goldman Sachs and JP Morgan and Morgan Stanley know exactly how their bread gets buttered, which is not by providing long-term accurate forecasts but by churning out fancy financial modelling in order to justify high fees from well-heeled clients. Geopolitical and biophysical realities play little to no part in their economic forecasts and other estimates, their assumptions of a short war effectively providing the requisite illusion for the continuation of profit making amidst business as usual and the delusion of living in an arrested and bucolic state of 2025. For were they to tell the truth, well, there's little reason not to think that their clients wouldn't panic, potentially leading to the bursting of the market bubble. So expect them to keep silent on the truth of the matter while continuing to dole out (at a cost!) the BS.

Financial traders don't get it, but commodity traders do... kind of

There's most certainly been a dearth of prominent individuals willing to call out the timelines of the aforementioned investment banks, one of the few doing so being the economist Jeff Currie. If you haven't caught him making the rounds on various podcasts and getting interviewed by various mainstream media outlets, Currie's been the one quick to take issue when presented with hypotheticals and assumptions about near-term solutions to the current crisis: "So, if this continues, if we see a blockade for another, let's say, two to four weeks—"

Wait, wait. I love how you say two to four weeks. Everybody has been saying two to four weeks since this started. [...] Where do you get your two to four weeks? You just randomly pull it out of thin air, just like everybody else, like these investment banks that are out going, “Don't worry, it'll be over within two to four weeks”.

Not merely "just like everybody else" though, but just like none other than US president Donald Trump himself who, via his repeated claims that a deal is just around the corner and that Iran is supposedly begging for a "deal", has been brazenly running the kind of pump and dump scheme that'd make even the highest of high-profile investment bankers blush.

To be clear, none of the above is to say that everybody other than Currie is BSing, nor that nobody on Wall Street or Bay Street or High Street or whatever Street understands the enormity and seriousness of the situation, just that the financial traders are largely ignorant of what's going on. For as Currie also stated,

Commodity traders understand the significance of the crisis. Financial traders do not understand the significance of the crisis.

Or as he explained it in more detail to CNBC,

So, the expectations are that, “Hey, we're going to get through this.” Um, I like to point out that none of these people touch bushels, barrels, or metric tons of any commodity. Every CEO – every oil company CEO, mining company CEO, every commodity trader – anybody who gets their hands dirty in this business is telling you “you have a problem”.

To a certain extent. Case in point here is the oilfield services firm Baker Hughes, whose assumption conveyed in its late-April financial guidance was based on the estimate that the conflict between the US and Iran would be settled sometime around late-June, albeit with acknowledgement that the Strait may not be fully operational until the second half of 2026.

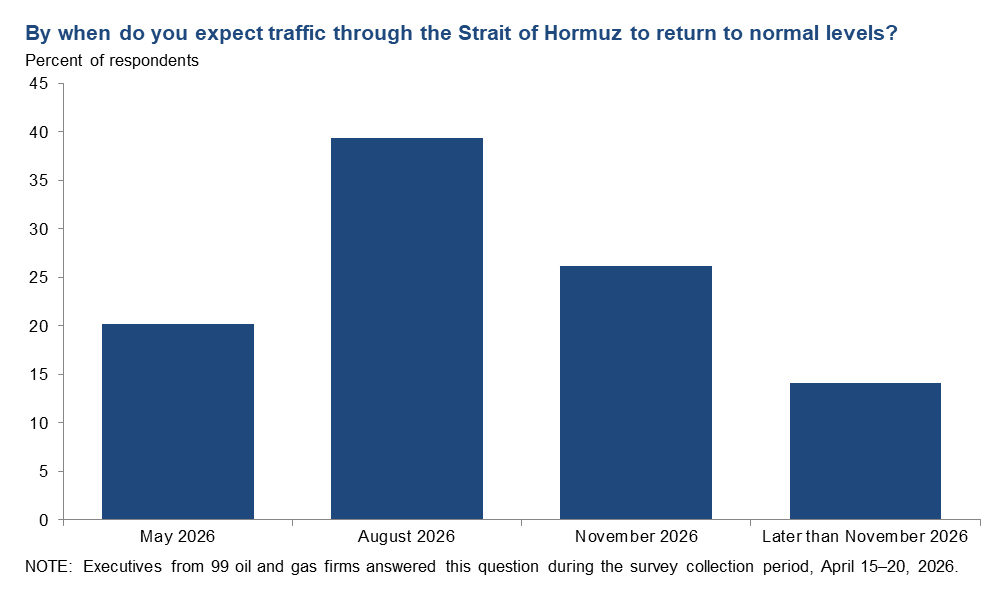

While the one-off assumption made by Baker Hughes didn't exactly fit with Currie's explanation, the Federal Reserve Bank of Dallas on the other hand took an across-the-board approach by surveying about 100 oil and gas executives between April 15th and 20th, all of whom were presented with a series of questions. The key question posed to them was the following: "By when do you expect traffic through the Strait of Hormuz to return to normal levels?"

- 20% answered by May

- 39% answered by August

- 25% answered by November

- 14% answered later than November

While a fifth of respondents somewhat disproved Currie's assessment by expecting traffic to resume even before the mythic month of June, one can perhaps be somewhat relieved to see that more than a third of oil and gas executives surveyed had not just the foresight but presumably enough of an understanding to not expect traffic through the Strait of Hormuz to return to "normal levels" until November or later.

While we'll get to why traffic through the Strait were never going to get back to "normal levels" by June (or even soon thereafter) some other time, in the meantime we'll look at one last instance of an energy investor – which is certainly different from an energy trader, the former being someone who takes a "buy-and-hold" approach by building wealth over years or decades, while the latter buys and sells assets and holds them for weeks or even mere seconds in order to exploit short-term price fluctuations – whose prognostications also fall under the rubric of delusional. That energy investor would be Eric Nuttall (which FF2F's previous post favourably included an embedded tweet by), lead portfolio manager of Ninepoint Energy Fund in Toronto and someone who similarly stated that the Strait of Hormuz situation can't possibly be allowed to escalate any further seeing how "the ramifications are so dramatic".

It's inevitable that the Strait will be opened. I would expect there to be a coalition. It's just the gravity of this is just – we're heading into a global mega recession if it's not, and so it has to, and it will be.

However, just like the dramatic ramifications of climate change aren't doing anything to curtail our usage of fossil fuels, the dramatic ramifications of inequality aren't doing anything to reign in skyrocketing wealth differentials, the dramatic ramifications on future food supplies aren't doing anything to halt biodiversity loss, etc., there's no supreme law of the universe that dictates that the Strait must open due to "the gravity of this", and that rather than heading for a depression we're instead merely headed for a "global mega recession". And that's not just due to possible worst-case scenarios that could very well eventuate.

Because while there's more than one party with agency in this war, Iranian state TV – whose every declaration is not necessarily mouthing state lines – published a graphic depicting energy facilities that would be targeted if/when the war resumes. In other words, while the Strait's eventual reopening is of course technically "inevitable", a reopening after a few rounds of highly destructive kinetic strikes in both directions could very well result in a reopening being essentially ineffectual if a great deal of physical production capacity in the Gulf is knocked out and is rendered unable to be turned back on very rapidly, if ever.

Nuttall certainly isn't the only individual with Pollyannaish attitudes as such, oil market researcher/analyst and fellow Torontonian Rory Johnston admitting that although JP Morgan's "depletion will ultimately force the reopening of the Strait of Hormuz, one way or another" analysis is "hand-wavey", it's nonetheless his opinion that "the cumulative consequences of Hormuz's closure will ultimately force its reopening". While not quite as "hand-wavey" as all the aforementioned "nothing this bad could possibly happen, therefore it won't happen"-esque statements, Johnston's opinion similarly seems to be imbued with what one might refer to as market determinism, as seen by his belief that "Trump has been thus far unwilling to make [...] concessions because there isn't enough market pressure to push him off his nuclear position".

Why the inclination towards the deterministic belief that geopolitics are ultimately trumped by signals given off by the market? While there's probably a slight touch of occupational superiority complex (whereby energy investors and oil market analysts see their fields – and markets in general – as being more consequential than any other fields), the overriding reason probably has more to do with blinders imposed by a preponderance towards normalcy bias: the expectation of an environment perpetually conducive to the insatiable desire for relatively predictable profit-making, clouding over even the consideration that unfolding events might not be conducive to the business as usual systemic stability necessary for meeting desires long grown accustomed to. All this is wonderfully exemplified by a recent tweet by Nuttall, one in which current (destructive) events are seen not as the opportunity for some kind of cultural renewal whereby current assumptions and practices are questioned, but rather as an "attractive entry point" for renewed profit making.

Which probably warrants some kind of update to the caption of that well-travelled 2012 editorial cartoon by cartoonist Tom Toro. (In which the boyish looks of the guy in the suit kinda looks like Nuttall?)

Base cases needn't be fairy tales

It's hardly an exaggeration to say that virtually all Strait of Hormuz watchers are spending most of their time pondering over when the Strait will be reopened (with perhaps a side of wondering what oil markets will look like once the day arrives), all the while focusing little to no time on analyzing what the situation might look like if the Strait doesn't reopen, or at least remains shut for a rather prolonged period of time. One of the very few individuals willing to consider such a possibility is retired petroleum geologist Art Berman, someone who doesn't see transit through the Strait of Hormuz normalizing until December of 2026.

Although it's not clear why Berman chose December for his base case normalization date, the timing suggests he might be assuming that the Islamic Revolutionary Guard Corps (IRGC) won't capitulate until after the US midterms are held (November 3rd), the potential defeat of Trump's MAGA Republicans in the House (and possibly also the Senate) leading not simply to Trump's impeachment but to what might effectively also be the IRGC's own version of regime change (providing somewhat of a retribution for the death of cleric and former supreme leader of Iran Ali Khamenei).

As interesting as taking a deeper look into Berman's base case may be, a far more interesting take on base cases would be that by Bloomberg energy and commodities columnist Javier Blas, whose late-May piece entitled "What If the Strait of Hormuz Didn’t Reopen?" largely paralleled much of what was written above by yours truly.

First off, Blas pointed out that most of his "contacts in the commodity and financial world [...] seem to think Hormuz will reopen next month [June], at worst in July", largely because "the consequences of the opposite happening – much higher energy prices and serious economic damage – are too painful to consider". Essentially what yours truly pointed out above, albeit via reports by various investments banks leaked out onto Twitter rather than via actual contacts in the industry. Alongside the preceding, Blas brought up what he described as a famous observation by American economist Herbert Stein, one in which it was stated that "If something cannot go on forever, it will stop". Again paralleling adaptations written above by yours truly, Blas tweaked the statement to parallel Wall Street's stance: "The Strait of Hormuz cannot be closed forever because it will cause too much economic damage. Therefore, it will reopen."

Blas also recounted the story of the Suez Canal's eight-year closure that began in 1967, stressing that although a repeat as such is "a nightmare few contemplate" and "is certainly not my own base case", it is however "a working example of just how long a blockade can drag on". Blas is therefore one of the few willing to consider that the situation could in fact get much worse over time, something that investment banks and news outlets have so far done their best to avoid contemplating.

So although Blas didn't offer any base case scenario of his own, he was however willing to question what would happen "if Hormuz stayed shut until late 2026, or into 2027? Or if the strait only opens partially", and even went so far as to give voice to the possibility that the Strait may not ever reopen.

Could the world live forever without the 10%-15% or so of its oil supply that Hormuz represents? Yes, but at vast cost. To cut consumption permanently by so much would most likely mean a global recession, as in the 1973 and 1979 oil crises.

We won't delve into what a world without much of the Middle East's oil (and helium and sulphur and natural gas and fertilisers) would look like, but suffice to say you certainly won't find the likes of Goldman Sachs, JP Morgan, Morgan Stanley, or any of the rest of them voicing issues as such in public, what with their very existence being predicated on business as usual running smoothly off into the sunset while they and all their clients are able to immerse themselves in the blissful illusion of being able to enjoy all the attendant creature comforts perpetually into the future. Or as Blas puts it, "Hormuz's long-term closure is so economically ruinous to contemplate that hardly anyone dares consider it".

Simply put, with the Strait currently closed, and with Trump's weekly pump and dump manipulation of the markets (and asinine threats on Truth Social) doing nothing to actually rectify the situation, if investors and their cohorts are going to regale us all with stories about the Strait's imminent reopening, then the burden of proof should rest on them to actually explain to us all why exactly that's going to happen without regressing into what are essentially vacuous and ridiculous expectations that the invisible hand of the market or what have you will wave its invisible magic wand that will magically rectify all hostilities, after which everybody can live happily ever after.

Investment banks of course aren't going to inhabit the real world and explain why exactly the Strait is going to open in "two to four weeks" or what have you, exemplified by those such as energy investor Eric Nuttall who are instead encouraging people (primarily fellow investors, one can presume), via the initial paragraph of a recent tweet, to ignore all the evidence before us and instead envision a day when we're all flipping peace signs to one another and passing around whatever it is that gets passed around in these circles.

Let's ignore the additional sea mine emplacing yesterday and just go with it...“the days away” peace deal is signed and the Strait is going to “open.” What is the most bearish scenario for oil???

And if that doesn't cut it, why not try closing our eyes and playing make believe games where we go to our happy places to dream about ponies and other wonderful things like lucrative investment opportunities.

An ambiguous base case

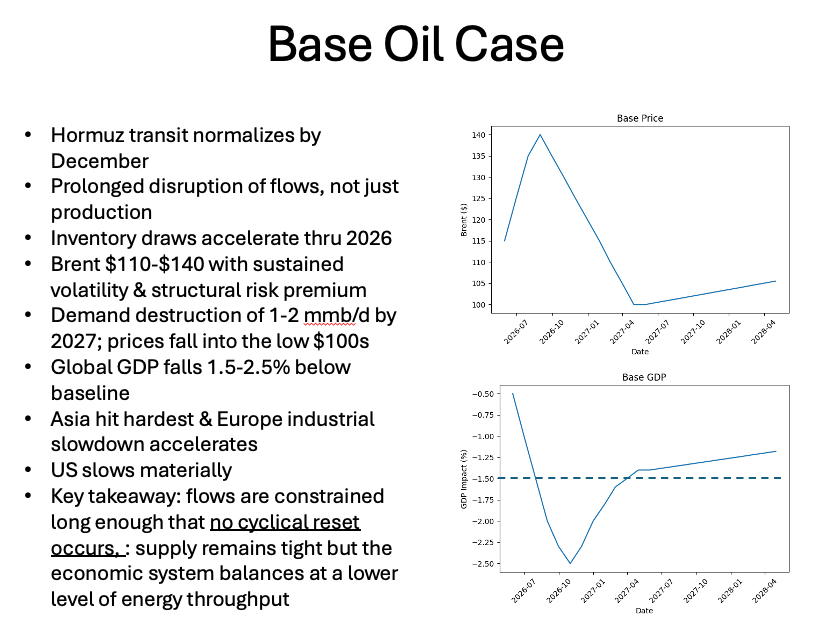

If you're thinking that this is the part where I offer my own base case then I'm sorry to say that you're going to be sorely disappointed, the lack of one partially being due to the fact that I lack the expertise to make a proper assessment of the situation from which I could assemble a cogent collection of conclusions (as seen in Berman's "Base Oil Case" image above). As a non-investor I will nonetheless state the following, which a good read of my outlook on the situation can rather easily be extracted from and applied to other parts of the economy.

If you're someone in the market for a new MacBook Pro, and are interested in the latest model – particularly in the M6-based revamped MacBook Ultra (or whatever it gets called) coming in late-2026 or early-2027 – you might want to be ready to pull the trigger for the current M5-based MacBook Pro, just in case. On the one hand, if the MacBook Ultra does in fact get released, it might be wise to purchase one as soon as it hits shelves. On the other hand, if word gets out that it's been delayed (due to the inability to manufacture the latest high-end computer chips, or for some other related reason), then it might be worthwhile to immediately settle for the latest M5-based MacBook Pro instead, while supplies last. Because it may very well be that once the latest batch of the M6-based MacBook Ultra or of the M5-based MacBook Pro is sold out, it could be a long time before a new batch of the latest and greatest is able to be manufactured again.

Extrapolate from that what you will.

Comments